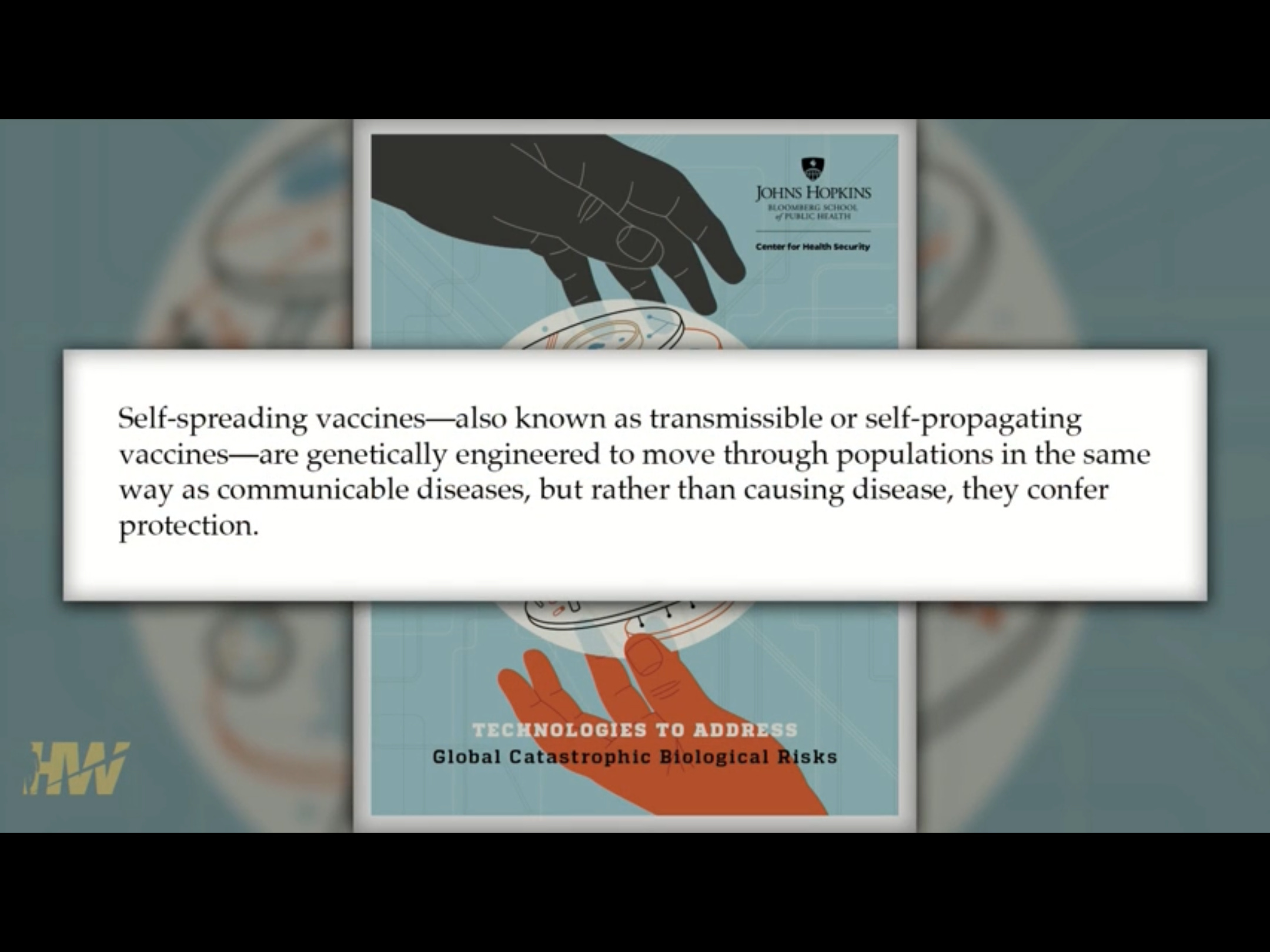

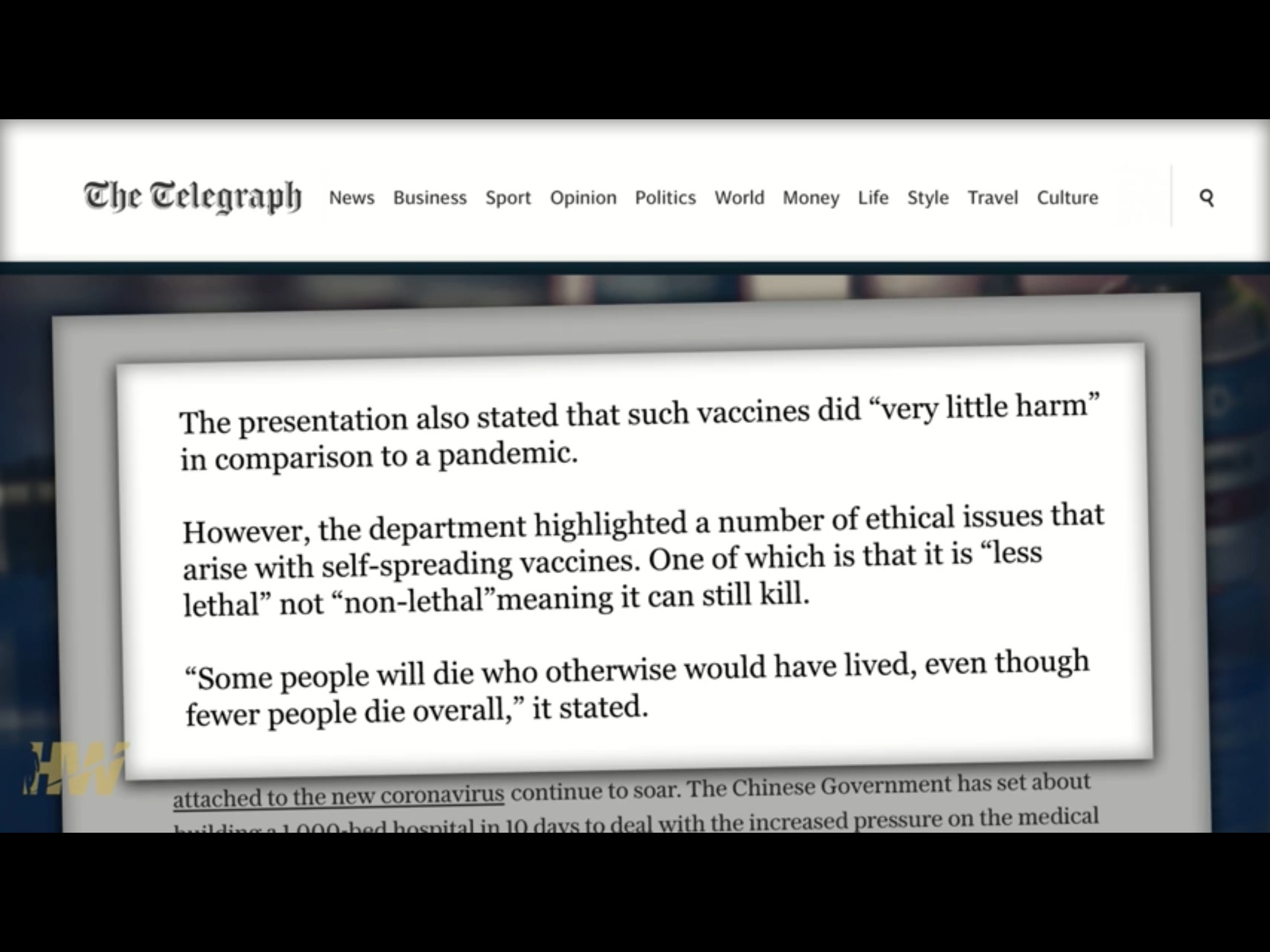

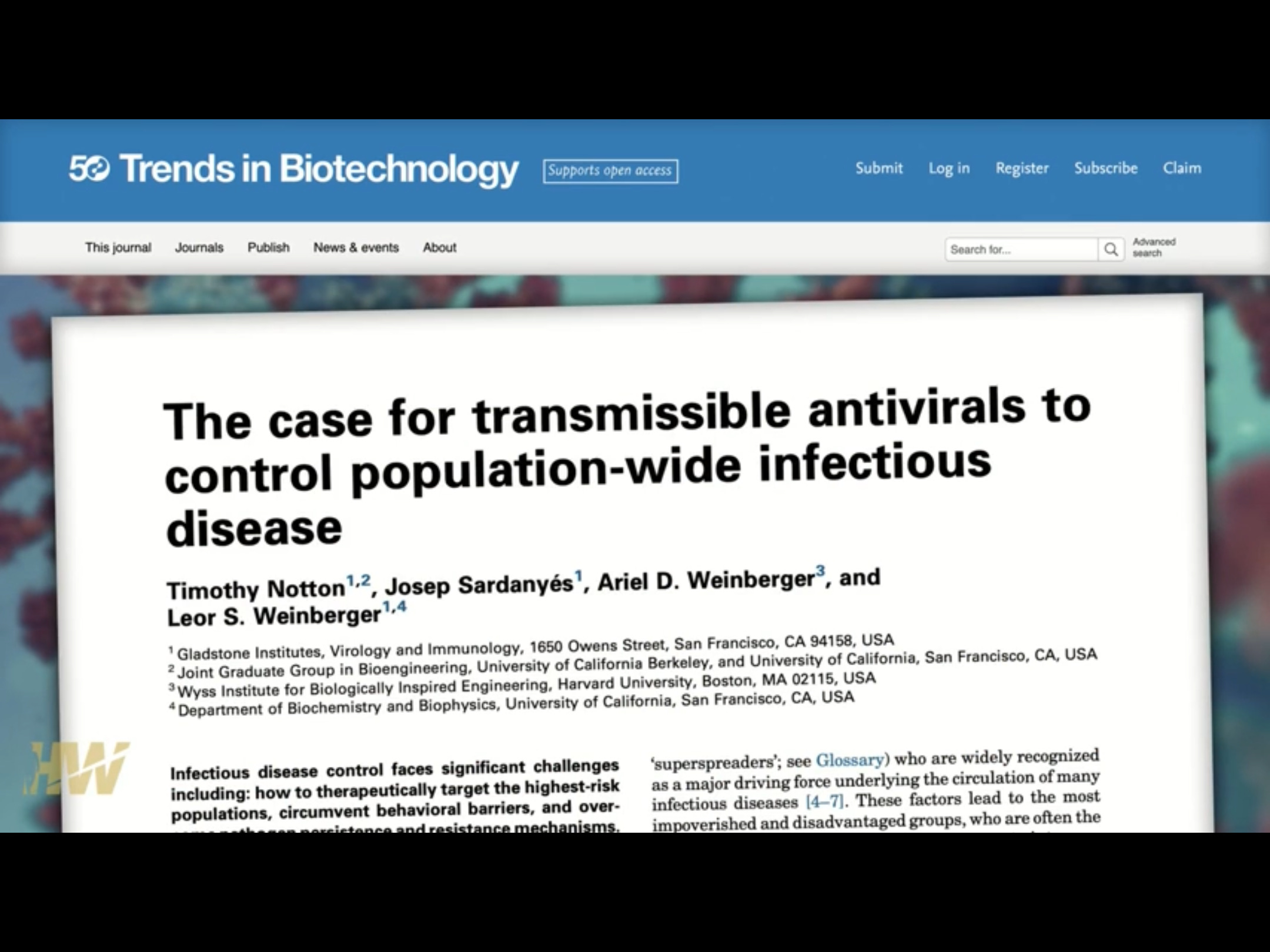

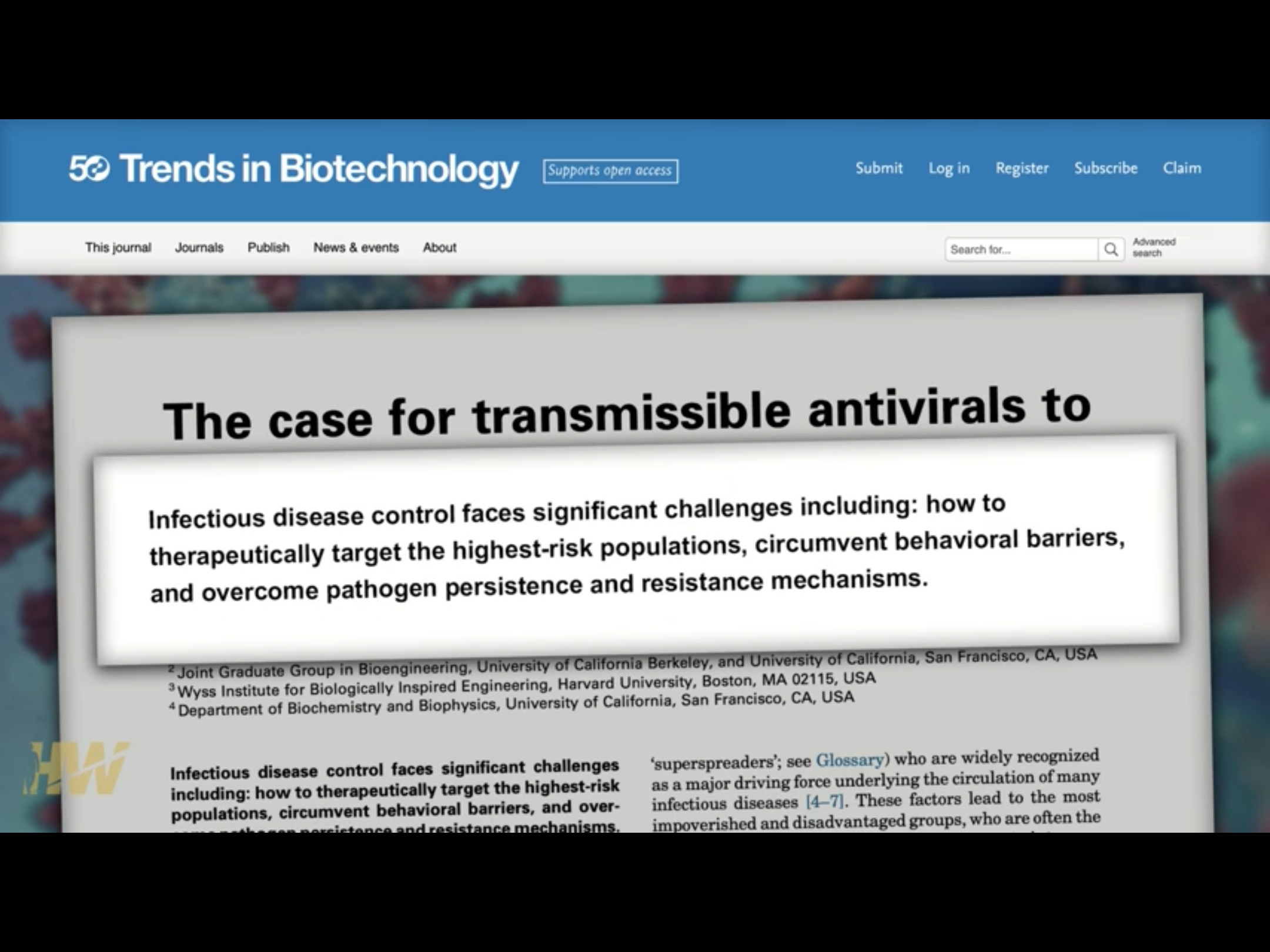

A new class of “encrypted RNA” vaccines are being developed where the

RNA would piggyback onto an existing wild virus and spread from person to person without any person’s knowledge or consent. Although this may

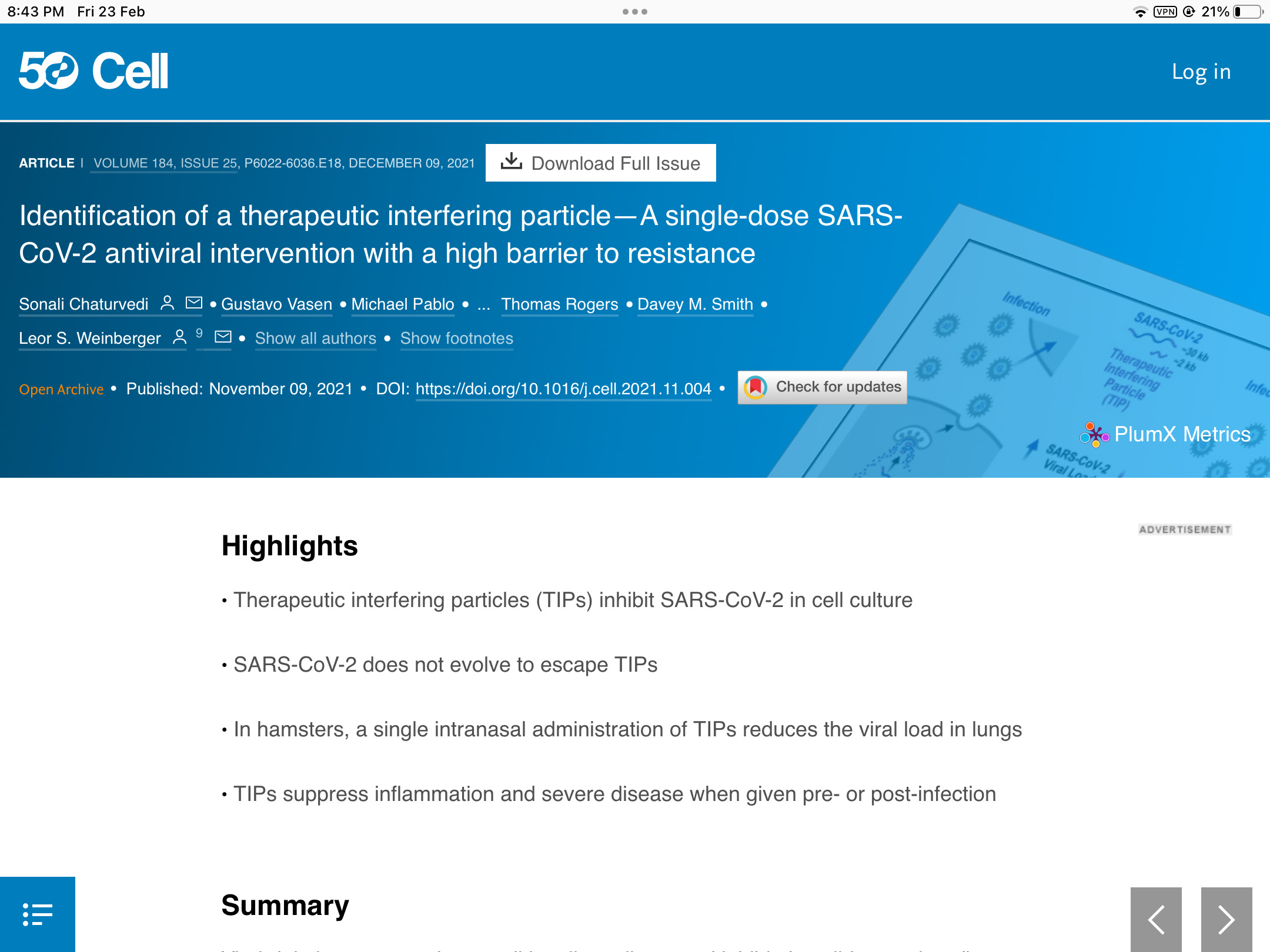

sound like science fiction, it is far from it. Two companies involved in this research have received millions of dollars from the federal government. A study using this technology on hamsters and the SARS-Cov-2 virus has already been completed and a Phase I trial on humans is in the works.

ICAN’s attorneys have already sent legal demands to all government

agencies involved.

It seems the government and the military are so enthused about this new vaccine deployment technology that Congress tucked a law, the PREVENT Pandemics Act, into the 2023 omnibus appropriations bill to facilitate it. Among other things, the Act has a section dedicated to Platform Technologies that supports the “development

and review of new treatments and countermeasures that use cutting-edge,

adaptable platform technologies that can be incorporated or used in more than one drug or biological product.”

https://pubmed.ncbi.nlm.nih.gov/25017994/

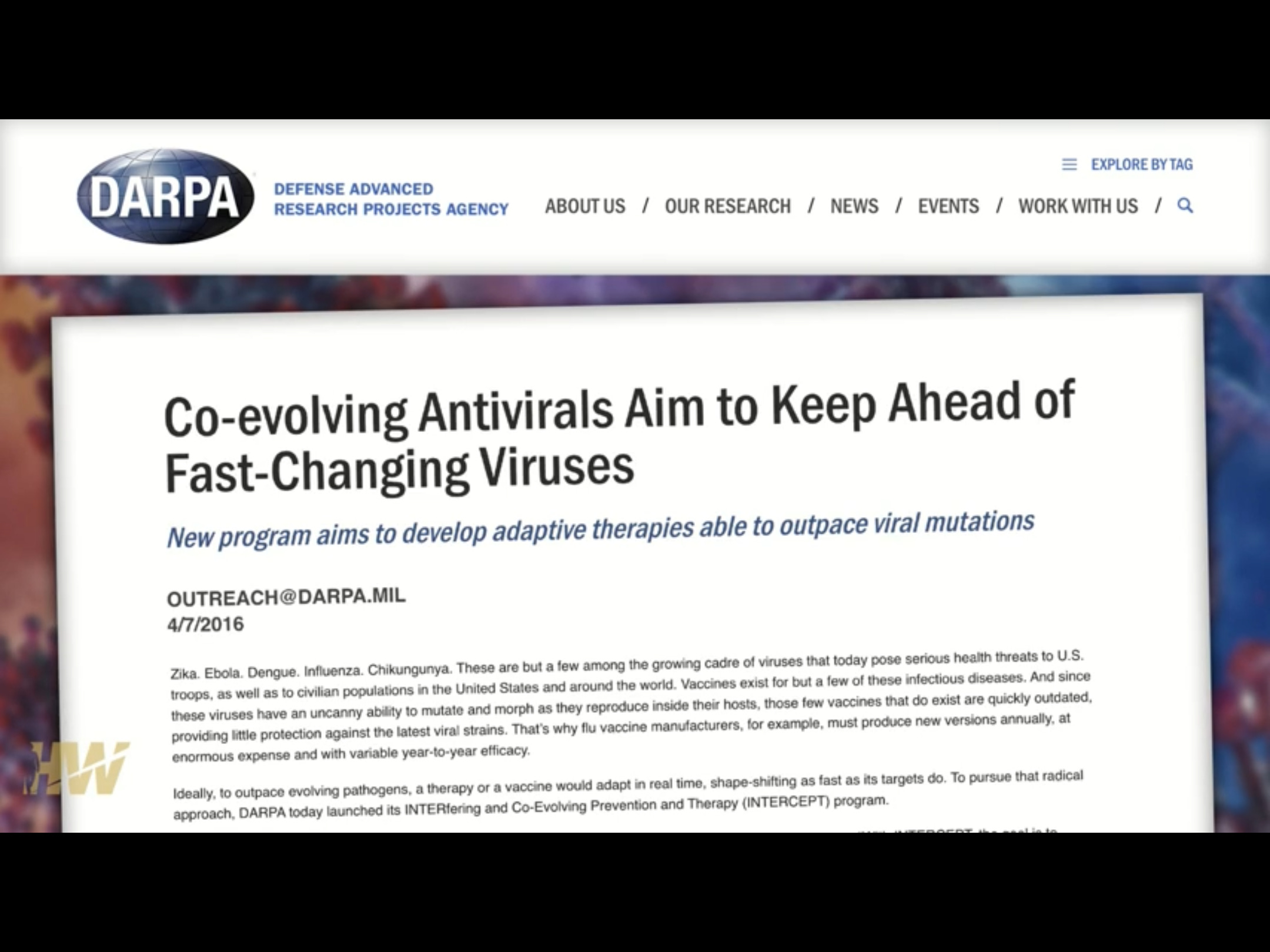

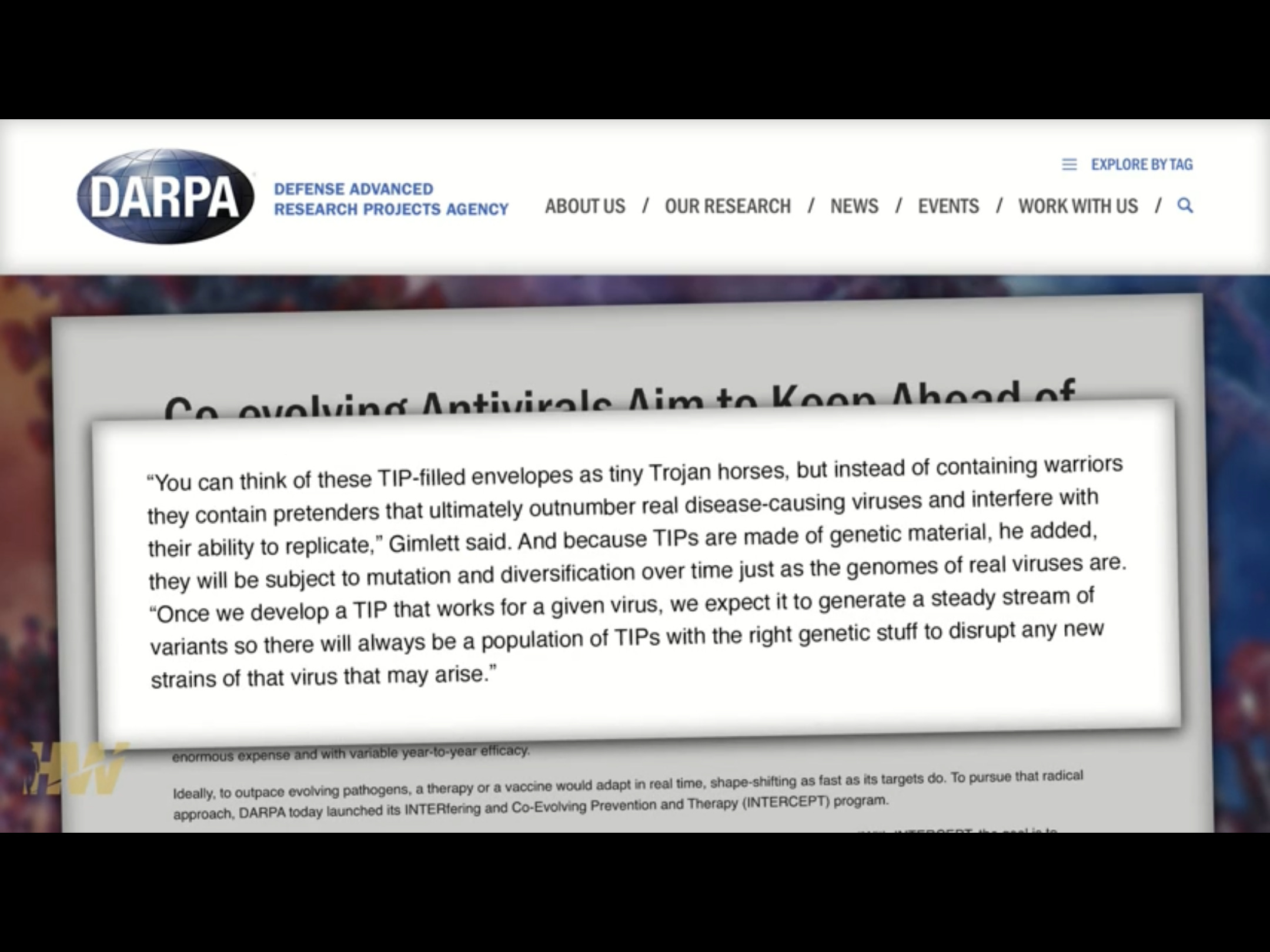

https://www.darpa.mil/news-events/2016-04-07a

This shows the official government interest

In 2020, and he is declaring victory over CreationCan we create vaccines that mutate and spread?

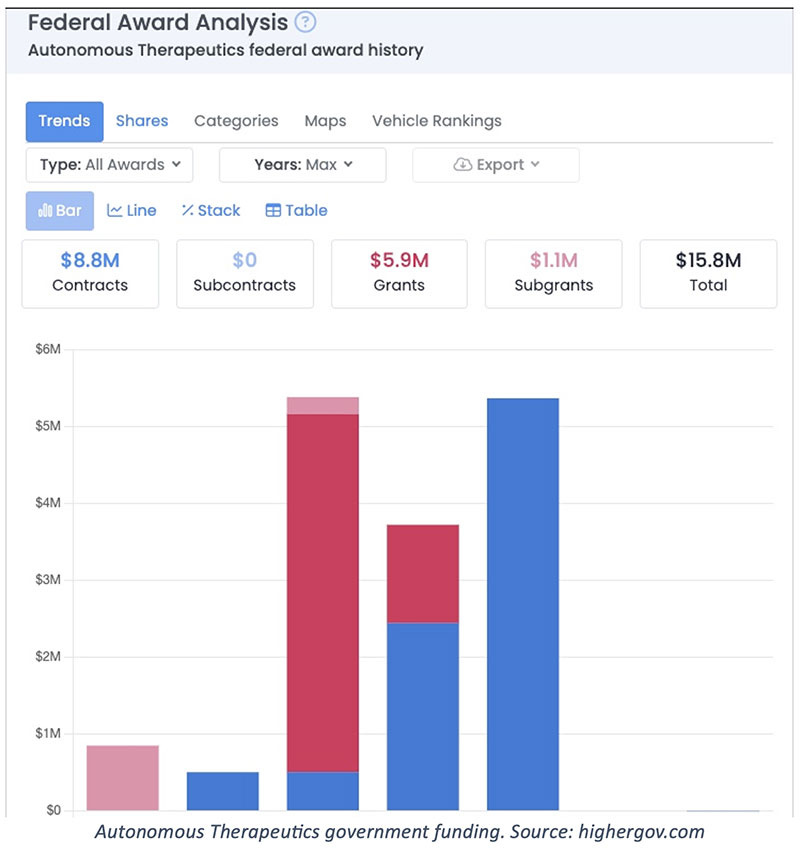

HHS issued a $4.8 million grant to VxBiosciences for “Autonomously Deploying,

Co-evolving SARS-CoV-2 Antiviral.” The grant was for engineering “therapeutic molecular parasites of SARS-CoV-2 that can co-adapt and transmit among infected hosts … acting as single-administration therapies that circumvent compliance issues.”

It seems the government and the military are so enthused about this new vaccine deployment technology that Congress tucked a law, the PREVENT Pandemics Act, into the 2023 omnibus appropriations bill to facilitate it. Among other things, the Act has a section dedicated to Platform Technologies that supports the “development and review of new treatments and countermeasures that use cutting-edge, adaptable platform technologies that can be incorporated or used in more

than one drug or biological product.”

Read the article HERE